Blank Promissory Note Template for California

Blank Promissory Note Template for California

In California, the Promissory Note form serves as a crucial document in lending transactions, providing a clear framework for the repayment of borrowed funds. This form outlines the terms of the loan, including the principal amount, interest rate, and repayment schedule, ensuring both the lender and borrower have a mutual understanding of their obligations. Essential elements such as the maturity date and any late payment penalties are also specified, creating a comprehensive agreement that protects the interests of both parties. The form may include provisions for prepayment, allowing borrowers the flexibility to pay off the loan early without incurring additional fees. Additionally, it typically requires the signatures of both the lender and borrower, solidifying the commitment to the terms laid out. By utilizing the Promissory Note, individuals and businesses can navigate the lending process with clarity and confidence, fostering trust and accountability in financial transactions.

Promissory Note Friendly Loan Agreement Format - A well-drafted note considers multiple future financial scenarios.

Promissory Note Friendly Loan Agreement Format - This form may also indicate whether the loan is to be repaid in installments or in a lump sum.

Washington Promissory Note - Repayment can be made in installments or as a lump sum, as specified in the document.

Once you have the California Promissory Note form in hand, it's time to fill it out carefully. Completing this form accurately is essential for establishing the terms of the loan agreement. Follow these steps to ensure you provide all necessary information.

After completing the form, review it for any errors or omissions. Once confirmed, distribute copies to all parties involved and keep a copy for your records. This ensures everyone has the necessary documentation for future reference.

When filling out and using the California Promissory Note form, keep these key points in mind:

Following these guidelines can help ensure a smooth lending experience.

Understanding the California Promissory Note form can be tricky. Many people have misconceptions about its purpose and requirements. Here are ten common misconceptions, along with clarifications to help you navigate this important financial document.

By understanding these misconceptions, individuals can better navigate the complexities of promissory notes in California. It is essential to approach these documents with accurate information to ensure all parties involved are protected and informed.

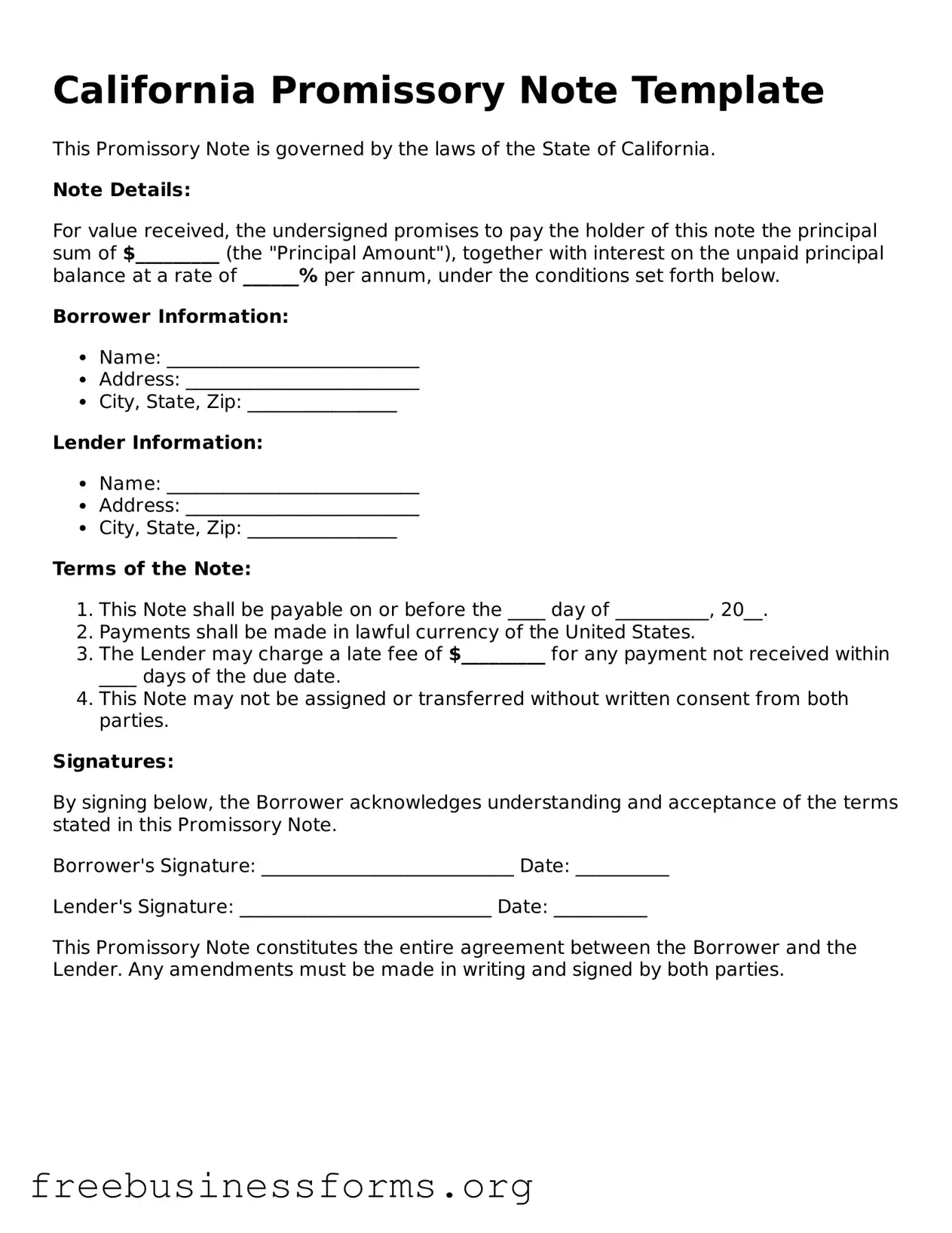

California Promissory Note Template

This Promissory Note is governed by the laws of the State of California.

Note Details:

For value received, the undersigned promises to pay the holder of this note the principal sum of $_________ (the "Principal Amount"), together with interest on the unpaid principal balance at a rate of ______% per annum, under the conditions set forth below.

Borrower Information:

Lender Information:

Terms of the Note:

Signatures:

By signing below, the Borrower acknowledges understanding and acceptance of the terms stated in this Promissory Note.

Borrower's Signature: ___________________________ Date: __________

Lender's Signature: ___________________________ Date: __________

This Promissory Note constitutes the entire agreement between the Borrower and the Lender. Any amendments must be made in writing and signed by both parties.

| Fact Name | Description |

|---|---|

| Definition | A California Promissory Note is a written promise to pay a specific amount of money to a designated person at a specified time. |

| Governing Law | The California Civil Code, specifically Sections 1901-1910, governs promissory notes in California. |

| Types | There are various types of promissory notes, including secured and unsecured notes, which differ based on whether collateral backs the loan. |

| Interest Rates | The interest rate on a promissory note can be fixed or variable, but it must comply with California's usury laws. |

| Signature Requirement | The borrower must sign the note for it to be legally binding. This signature indicates agreement to the terms outlined in the document. |

| Enforceability | Promissory notes are generally enforceable in court, provided they meet the legal requirements set forth in California law. |

| Default Consequences | If the borrower defaults, the lender has the right to pursue legal action to recover the owed amount, along with any applicable fees or interest. |