Official Cg 20 10 07 04 Liability Endorsement Form in PDF

Official Cg 20 10 07 04 Liability Endorsement Form in PDF

The CG 20 10 07 04 Liability Endorsement form is a critical component of commercial general liability insurance, specifically designed to extend coverage to additional insured parties such as owners, lessees, or contractors. This endorsement modifies the existing policy, ensuring that those listed in the endorsement schedule are protected against liabilities related to bodily injury, property damage, or personal and advertising injury that may arise from the insured's operations. It is essential to understand that the coverage applies only to the extent permitted by law and is limited to the obligations outlined in any applicable contracts or agreements. Notably, the endorsement includes specific exclusions that clarify when coverage is not applicable, particularly in scenarios where work has been completed or where the injury or damage occurs after the project has been put to its intended use. Additionally, the limits of insurance for the additional insured are capped at either the amount required by the contract or the available limits of the policy, whichever is less. This nuanced approach ensures that all parties have a clear understanding of their coverage while maintaining compliance with contractual obligations.

Share Transfer Form - Utilize for internal reporting on stock ownership and transfers.

Hub Certification Texas - This form streamlines the administrative tasks of membership management.

Printable Time Card - Be punctual when turning in your time card.

Filling out the CG 20 10 07 04 Liability Endorsement form requires careful attention to detail. This form is essential for adding additional insured parties to your commercial general liability policy. It is important to ensure that all information is accurate and complete to avoid any issues with coverage.

Here are some key takeaways regarding the Cg 20 10 07 04 Liability Endorsement form:

Understanding the CG 20 10 07 04 Liability Endorsement form is essential for those involved in commercial insurance. However, several misconceptions often arise. Here are nine common misunderstandings:

By clarifying these misconceptions, individuals can better navigate their insurance needs and ensure they have the appropriate coverage for their operations.

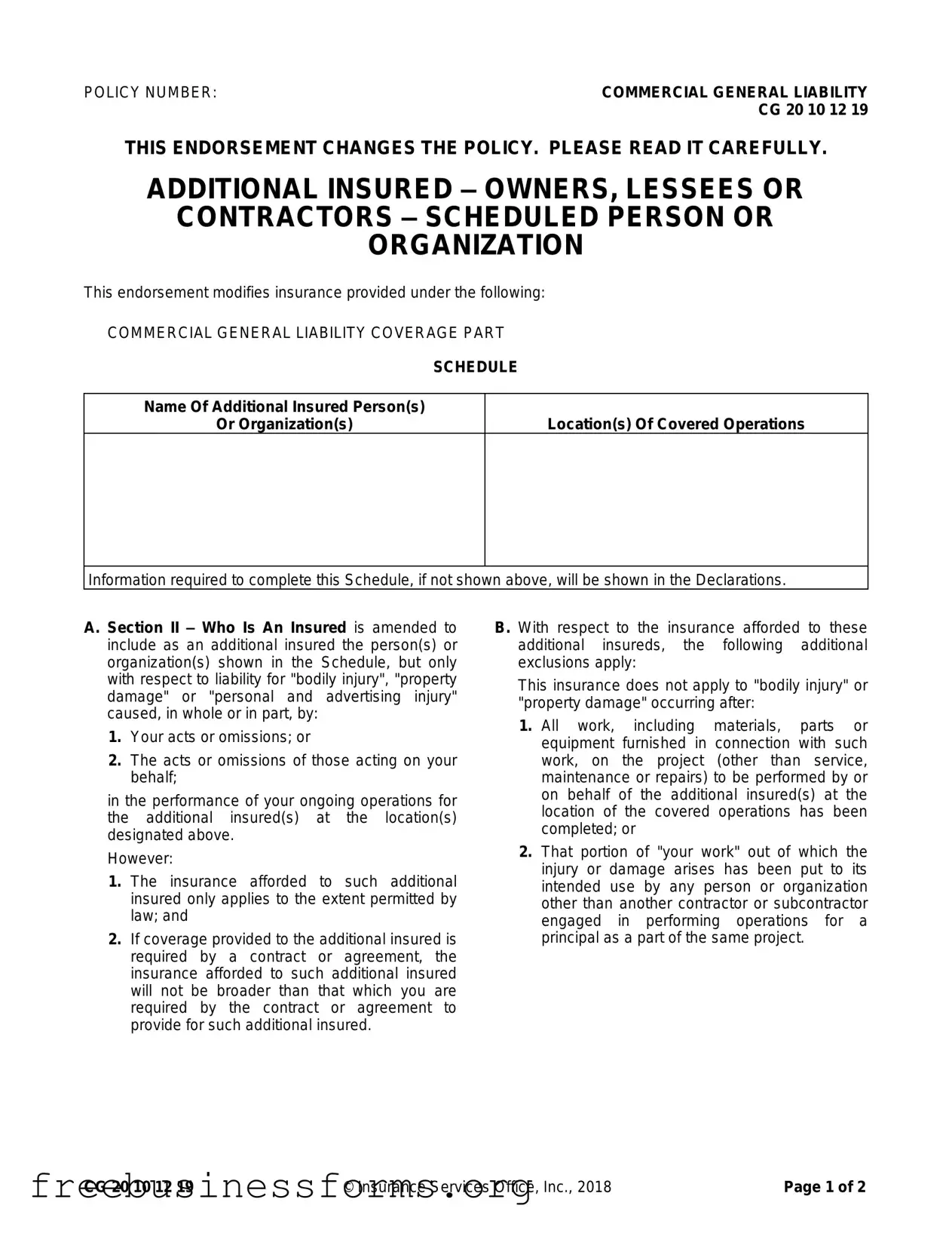

POLICY NUMBER: |

COMMERCIAL GENERAL LIABILITY |

|

CG 20 10 12 19 |

THIS ENDORSEMENT CHANGES THE POLICY. PLEASE READ IT CAREFULLY.

ADDITIONAL INSURED – OWNERS, LESSEES OR

CONTRACTORS – SCHEDULED PERSON OR

ORGANIZATION

This endorsement modifies insurance provided under the following:

COMMERCIAL GENERAL LIABILITY COVERAGE PART

SCHEDULE

Name Of Additional Insured Person(s)

Or Organization(s)

Location(s) Of Covered Operations

Information required to complete this Schedule, if not shown above, will be shown in the Declarations.

A. Section II – Who Is An Insured is amended to include as an additional insured the person(s) or organization(s) shown in the Schedule, but only with respect to liability for "bodily injury", "property damage" or "personal and advertising injury" caused, in whole or in part, by:

1.Your acts or omissions; or

2.The acts or omissions of those acting on your behalf;

in the performance of your ongoing operations for the additional insured(s) at the location(s) designated above.

However:

1.The insurance afforded to such additional insured only applies to the extent permitted by law; and

2.If coverage provided to the additional insured is required by a contract or agreement, the insurance afforded to such additional insured will not be broader than that which you are required by the contract or agreement to provide for such additional insured.

B. With respect to the insurance afforded to these additional insureds, the following additional exclusions apply:

This insurance does not apply to "bodily injury" or "property damage" occurring after:

1.All work, including materials, parts or equipment furnished in connection with such work, on the project (other than service, maintenance or repairs) to be performed by or on behalf of the additional insured(s) at the location of the covered operations has been completed; or

2.That portion of "your work" out of which the injury or damage arises has been put to its intended use by any person or organization other than another contractor or subcontractor engaged in performing operations for a principal as a part of the same project.

CG 20 10 12 19 |

© Insurance Services Office, Inc., 2018 |

Page 1 of 2 |

C. With respect to the insurance afforded to these additional insureds, the following is added to

Section III – Limits Of Insurance:

If coverage provided to the additional insured is required by a contract or agreement, the most we will pay on behalf of the additional insured is the amount of insurance:

1.Required by the contract or agreement; or

2.Available under the applicable limits of insurance;

whichever is less.

This endorsement shall not increase the applicable limits of insurance.

Page 2 of 2 |

© Insurance Services Office, Inc., 2018 |

CG 20 10 12 19 |

| Fact Name | Description |

|---|---|

| Policy Number | The endorsement is identified as CG 20 10 12 19, which is a part of the Commercial General Liability (CGL) policy. |

| Purpose | This endorsement adds additional insureds, specifically owners, lessees, or contractors, to the policy. |

| Coverage Scope | It covers liability for bodily injury, property damage, or personal and advertising injury linked to the insured's operations. |

| Location Specificity | Coverage is limited to specific locations where the additional insured's operations occur, as outlined in the schedule. |

| Legal Limitations | The insurance applies only to the extent permitted by law, ensuring compliance with state regulations. |

| Contractual Obligations | If required by a contract, coverage cannot exceed what is stipulated in that agreement for the additional insured. |

| Exclusions | Coverage does not apply if the injury or damage occurs after the project work has been completed. |

| Limit of Insurance | The maximum amount payable on behalf of the additional insured is the lesser of the contract amount or the policy limits. |

| Endorsement Modification | This endorsement modifies the existing insurance policy, and it is crucial to read it carefully to understand its implications. |