Blank Loan Agreement Template for Illinois

Blank Loan Agreement Template for Illinois

The Illinois Loan Agreement form is a crucial document that outlines the terms and conditions of a loan between a lender and a borrower. This form typically includes essential details such as the loan amount, interest rate, repayment schedule, and any collateral involved. It serves to protect both parties by clearly stating their rights and obligations. Additionally, the agreement may specify the consequences of default, including late fees or legal action. Understanding each section of the form is vital, as it ensures that both the lender and borrower are on the same page regarding their financial arrangement. By using this form, individuals can avoid misunderstandings and foster a transparent lending process.

Georgia Promissory Note - Details about any grace periods or payment holidays may be included.

Texas Promissory Note Requirements - Specifies the loan amount, interest rates, and repayment schedule.

New York Promissory Note - This document can play a key role in personal finance and budget planning.

Loan Note Template - A Loan Agreement can be tailored to fit the needs of both the lender and the borrower.

Once you have the Illinois Loan Agreement form in front of you, it’s time to get started on filling it out. Follow these steps carefully to ensure all necessary information is provided accurately.

With the form completed, you can now proceed to share it with the relevant parties. Make sure to keep a copy for your records.

When dealing with the Illinois Loan Agreement form, it's important to understand several key aspects to ensure a smooth process. Here are four essential takeaways:

By following these guidelines, you can navigate the Illinois Loan Agreement process with confidence and minimize potential complications.

Understanding the Illinois Loan Agreement form is crucial for both lenders and borrowers. However, several misconceptions can lead to confusion. Here are eight common misconceptions explained:

By understanding these misconceptions, both lenders and borrowers can better navigate the loan process and protect their interests.

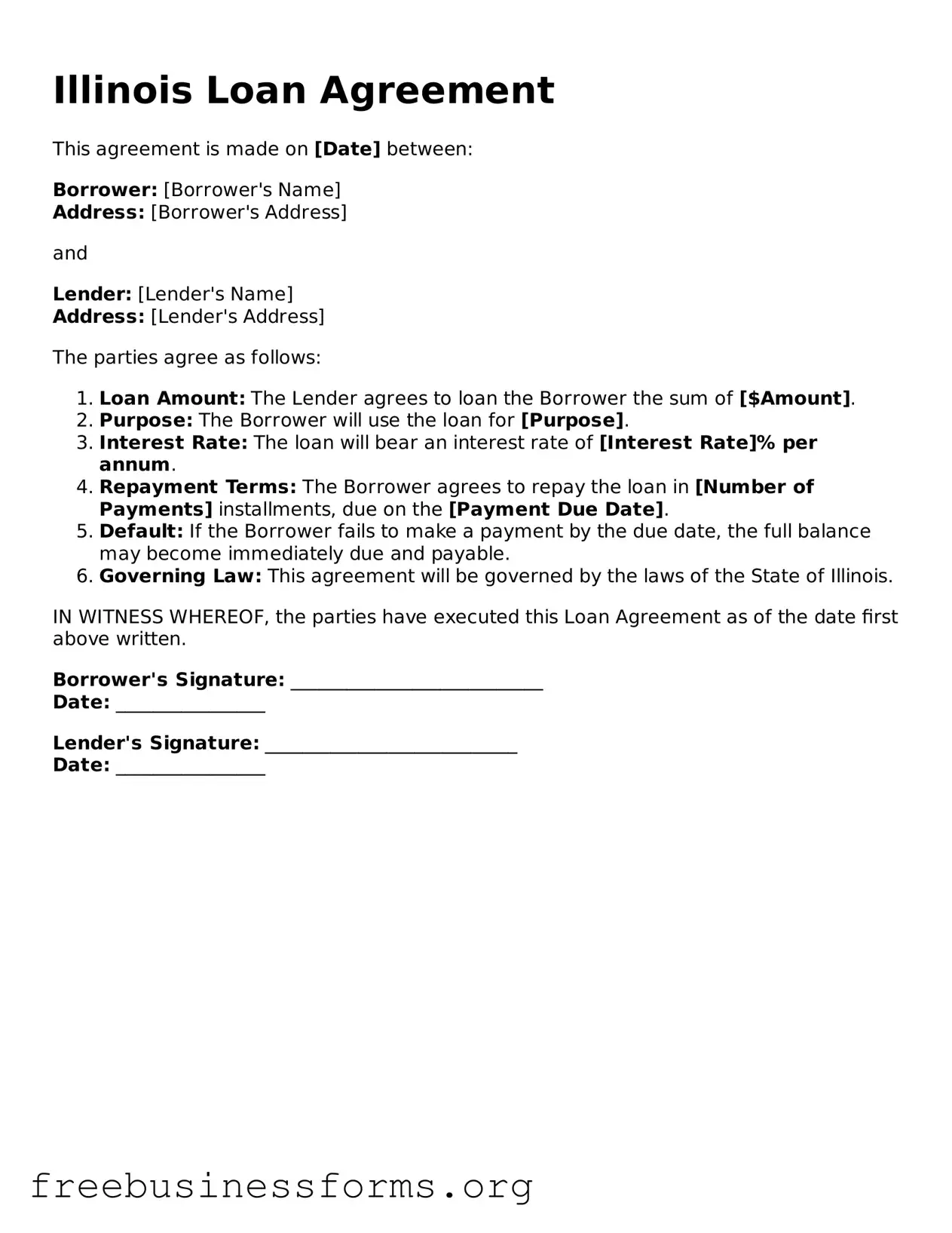

Illinois Loan Agreement

This agreement is made on [Date] between:

Borrower: [Borrower's Name]

Address: [Borrower's Address]

and

Lender: [Lender's Name]

Address: [Lender's Address]

The parties agree as follows:

IN WITNESS WHEREOF, the parties have executed this Loan Agreement as of the date first above written.

Borrower's Signature: ___________________________

Date: ________________

Lender's Signature: ___________________________

Date: ________________

| Fact Name | Details |

|---|---|

| Purpose | The Illinois Loan Agreement form is used to outline the terms of a loan between a lender and a borrower, ensuring clarity and legal protection for both parties. |

| Governing Law | This agreement is governed by the laws of the State of Illinois, specifically under the Illinois Compiled Statutes. |

| Essential Elements | Key components include the loan amount, interest rate, repayment schedule, and any collateral involved. |

| Signatures | Both the lender and borrower must sign the agreement to make it legally binding, indicating their acceptance of the terms. |