Official Mortgage Statement Form in PDF

Official Mortgage Statement Form in PDF

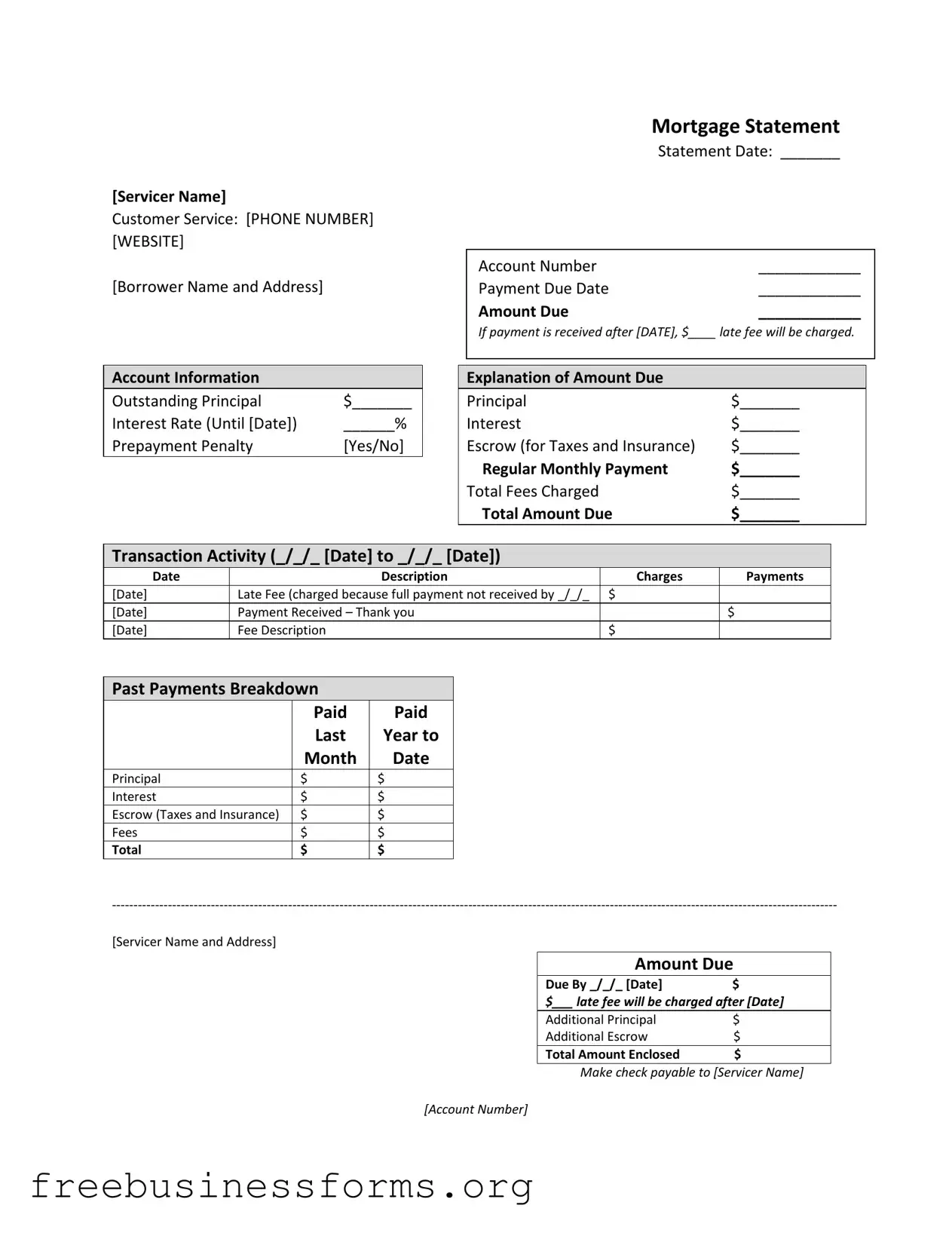

The Mortgage Statement form serves as a crucial document for homeowners, providing a detailed overview of their mortgage account. At the top of the form, the servicer's name and contact information, including a phone number and website, are prominently displayed for easy access to customer service. Below this, the borrower's name and address are listed, alongside essential details such as the statement date, account number, payment due date, and the total amount due. If a payment is not received by the specified date, the form indicates that a late fee will be charged. Key account information follows, highlighting the outstanding principal balance, interest rate, and whether a prepayment penalty applies. The form breaks down the amount due into categories like principal, interest, and escrow for taxes and insurance, culminating in the total fees charged. Transaction activity is documented over a specified period, detailing any charges, payments, and late fees incurred. Additionally, past payments are summarized to provide a clear picture of the borrower's payment history. Important messages regarding partial payments and delinquency notices are included, alerting borrowers to potential consequences of late payments. Finally, resources for those experiencing financial difficulty are noted, encouraging homeowners to seek assistance if needed.

Da - Can be used for both individual items and bulk property transfers.

Melaleuca Membership Cancellation Form - Melaleuca values its customers and appreciates the time taken to share your insights.

Da638 - The purpose of the form aligns with Army Regulation 600-8-22.

Completing the Mortgage Statement form is a straightforward process that requires careful attention to detail. This form includes important information about your mortgage account, including payment due dates and outstanding balances. Follow the steps below to accurately fill out the form.

After completing the form, double-check all entries for accuracy. Ensure that all required fields are filled out correctly before submitting it to the mortgage servicer. This will help avoid any delays or issues with your mortgage account.

When filling out and using the Mortgage Statement form, consider the following key takeaways:

There are several misconceptions about the Mortgage Statement form that can lead to confusion for borrowers. Understanding these can help clarify the information presented and ensure timely payments. Below are eight common misconceptions:

Understanding these misconceptions can help borrowers navigate their mortgage statements more effectively and make informed financial decisions.

[Servicer Name]

Customer Service: [PHONE NUMBER] [WEBSITE]

[Borrower Name and Address]

Mortgage Statement

Statement Date: _______

Account Number |

____________ |

Payment Due Date |

____________ |

Amount Due |

____________ |

If payment is received after [DATE], $____ late fee will be charged.

Account Information

Outstanding Principal |

$_______ |

Interest Rate (Until [Date]) |

______% |

Prepayment Penalty |

[Yes/No] |

Explanation of Amount Due

Principal |

$_______ |

Interest |

$_______ |

Escrow (for Taxes and Insurance) |

$_______ |

Regular Monthly Payment |

$_______ |

Total Fees Charged |

$_______ |

Total Amount Due |

$_______ |

Transaction Activity (_/_/_ [Date] to _/_/_ [Date])

Date |

Description |

Charges |

Payments |

[Date] |

Late Fee (charged because full payment not received by _/_/_ |

$ |

|

[Date] |

Payment Received – Thank you |

|

$ |

[Date] |

Fee Description |

$ |

|

Past Payments Breakdown

|

Paid |

Paid |

|

Last |

Year to |

|

Month |

Date |

Principal |

$ |

$ |

Interest |

$ |

$ |

Escrow (Taxes and Insurance) |

$ |

$ |

Fees |

$ |

$ |

Total |

$ |

$ |

[Servicer Name and Address]

Amount Due

Due By _/_/_ [Date]$

$___ late fee will be charged after [Date]

Additional Principal |

$ |

Additional Escrow |

$ |

Total Amount Enclosed |

$ |

Make check payable to [Servicer Name]

[Account Number]

[Additional tables to be translated]

Important Messages

*Partial Payments: Any partial payments that you make are not applied to your mortgage, but instead are held in a separate suspense account. If you pay the balance of a partial payment, the funds will then be applied to your mortgage.

**Delinquency Notice**

You are late on your mortgage payments. Failure to bring your loan current may result in fees and foreclosure – the loss of your home. As of [Date], you are __ days delinquent on your mortgage loan.

Recent Account History

·Payment due [Date]: Fully paid on time

·Payment due [Date]: Fully paid on [Date]

·Payment due [Date]: Unpaid balance of $________

·Current payment due [Date]: $_______

·Total: $_______ due. You must pay this amount to bring your loan current.

If you are Experiencing Financial Difficulty: See back for information about mortgage counseling or assistance.

| Fact Name | Description |

|---|---|

| Servicer Information | The mortgage statement includes the servicer's name, customer service phone number, and website for borrower inquiries. |

| Account Details | Key account information such as outstanding principal, interest rate, and prepayment penalty status is clearly outlined. |

| Payment Information | The statement specifies the payment due date, amount due, and any applicable late fees if payment is not received on time. |

| Delinquency Notice | A notice alerts borrowers if they are late on payments, detailing the potential consequences, including fees and foreclosure risks. |