Official Profit And Loss Form in PDF

Official Profit And Loss Form in PDF

The Profit and Loss form is a crucial tool for any business, providing a clear snapshot of financial performance over a specific period. This form details revenue, costs, and expenses, allowing business owners to understand their profitability. By breaking down income sources and categorizing expenditures, the Profit and Loss form enables easy identification of trends and areas for improvement. It serves not only as a historical record but also as a valuable resource for future planning and decision-making. With accurate data, businesses can assess their financial health, make informed choices, and strategize for growth. Understanding this form is essential for entrepreneurs and stakeholders alike, as it highlights the relationship between income and expenses, ultimately influencing the overall success of the enterprise.

Melaleuca Membership Cancellation Form - It is designed to be straightforward to ensure ease of use for all customers.

Employer's Quarterly Federal Tax Return - Employers can avoid common mistakes in Form 941 by adhering to IRS guidelines.

To successfully complete the Profit And Loss form, you will need to gather your financial information for the specified period. This will help you accurately report your income and expenses. Follow the steps below to fill out the form correctly.

Once you have completed these steps, you will have a filled-out Profit And Loss form ready for submission or record-keeping.

Filling out and using a Profit and Loss (P&L) form is crucial for understanding the financial health of a business. Here are some key takeaways to keep in mind:

By keeping these points in mind, you can effectively use the Profit and Loss form to make informed decisions for your business.

Understanding the Profit and Loss (P&L) form is essential for anyone involved in managing finances. However, several misconceptions can lead to confusion. Here’s a list of common misunderstandings about the P&L form:

By clearing up these misconceptions, individuals can better understand the importance of the Profit and Loss form and how it impacts overall business management.

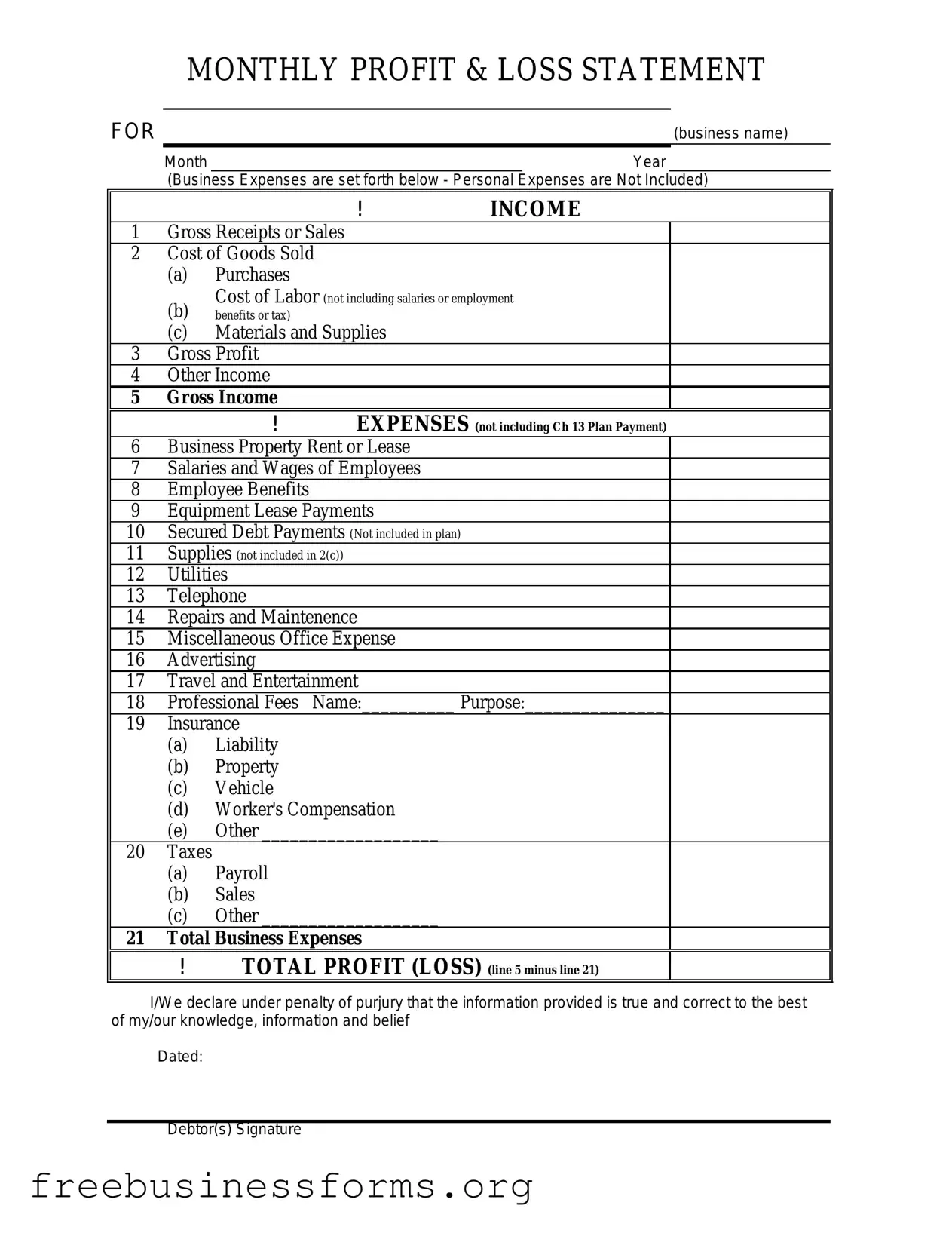

MONTHLY PROFIT & LOSS STATEMENT

FOR |

(business name) |

Month |

Year |

(Business Expenses are set forth below - Personal Expenses are Not Included)

|

|

|

! |

INCOME |

1 |

Gross Receipts or Sales |

|

||

2 |

Cost of Goods Sold |

|

||

|

(a) |

Purchases |

|

|

|

(b) |

Cost of Labor (not including salaries or employment |

||

|

benefits or tax) |

|

|

|

|

(c) |

Materials and Supplies |

|

|

3 |

Gross Profit |

|

|

|

4 |

Other Income |

|

|

|

5 |

Gross Income |

EXPENSES (not including Ch 13 Plan Payment) |

||

|

|

! |

||

6 |

Business Property Rent or Lease |

|

||

7 |

Salaries and Wages of Employees |

|

||

8 |

Employee Benefits |

|

|

|

9 |

Equipment Lease Payments |

|

||

10 |

Secured Debt Payments (Not included in plan) |

|

||

11 |

Supplies (not included in 2(c)) |

|

||

12 |

Utilities |

|

|

|

13 |

Telephone |

|

|

|

14 |

Repairs and Maintenence |

|

||

15 |

Miscellaneous Office Expense |

|

||

16 |

Advertising |

|

|

|

17 |

Travel and Entertainment |

|

||

18 |

Professional Fees |

Name:__________ Purpose:_______________ |

||

19 |

Insurance |

|

|

|

|

(a) |

Liability |

|

|

|

(b) |

Property |

|

|

|

(c) |

Vehicle |

|

|

|

(d) |

Worker's Compensation |

|

|

|

(e) |

Other ___________________ |

|

|

20 |

Taxes |

|

|

|

|

(a) |

Payroll |

|

|

|

(b) |

Sales |

|

|

|

(c) |

Other ___________________ |

|

|

21 |

Total Business Expenses |

|

||

|

! |

TOTAL PROFIT (LOSS) (line 5 minus line 21) |

||

I/We declare under penalty of purjury that the information provided is true and correct to the best of my/our knowledge, information and belief

Dated:

Debtor(s) Signature

| Fact Name | Description |

|---|---|

| Purpose | The Profit and Loss form summarizes a company's revenues, costs, and expenses over a specific period, helping to assess financial performance. |

| Key Components | This form typically includes sections for gross income, operating expenses, and net profit or loss. |

| Filing Requirements | Businesses may need to submit this form annually or quarterly, depending on state regulations and the type of business entity. |

| Governing Laws | In California, for instance, the form is governed by the California Corporations Code, while in New York, it falls under the New York Business Corporation Law. |