Official Promissory Note Form

Official Promissory Note Form

When it comes to financial transactions, a Promissory Note serves as a critical tool that outlines the terms of a loan agreement between a borrower and a lender. This legally binding document details the amount borrowed, the interest rate, and the repayment schedule, ensuring that both parties have a clear understanding of their obligations. In addition to these essential elements, the Promissory Note also specifies the consequences of default, providing a layer of security for the lender. It can be customized to include provisions such as prepayment options and collateral requirements, making it a versatile instrument for various lending scenarios. By formalizing the agreement in writing, the Promissory Note helps to prevent misunderstandings and disputes, fostering trust between the parties involved. Given the importance of this document in both personal and commercial lending, understanding its structure and implications is vital for anyone engaged in borrowing or lending money.

Jet Ski Trailer Bill of Sale - The sale documentation can aid in future repairs or service requests.

Mobile Home Clipart - A Mobile Home Bill of Sale can be used in various jurisdictions across the U.S.

Completing the Promissory Note form requires careful attention to detail. Once filled out correctly, the form will serve as a formal agreement between the parties involved. Follow the steps below to ensure accuracy and clarity.

After completing the form, ensure that both parties retain a copy for their records. This will help in maintaining clear communication and accountability moving forward.

When filling out and using a Promissory Note form, keep these key takeaways in mind:

Understanding the Promissory Note form can be challenging due to various misconceptions. Here are ten common misunderstandings about this important financial document:

By clarifying these misconceptions, individuals can better navigate the complexities of promissory notes and ensure they are used effectively in their financial dealings.

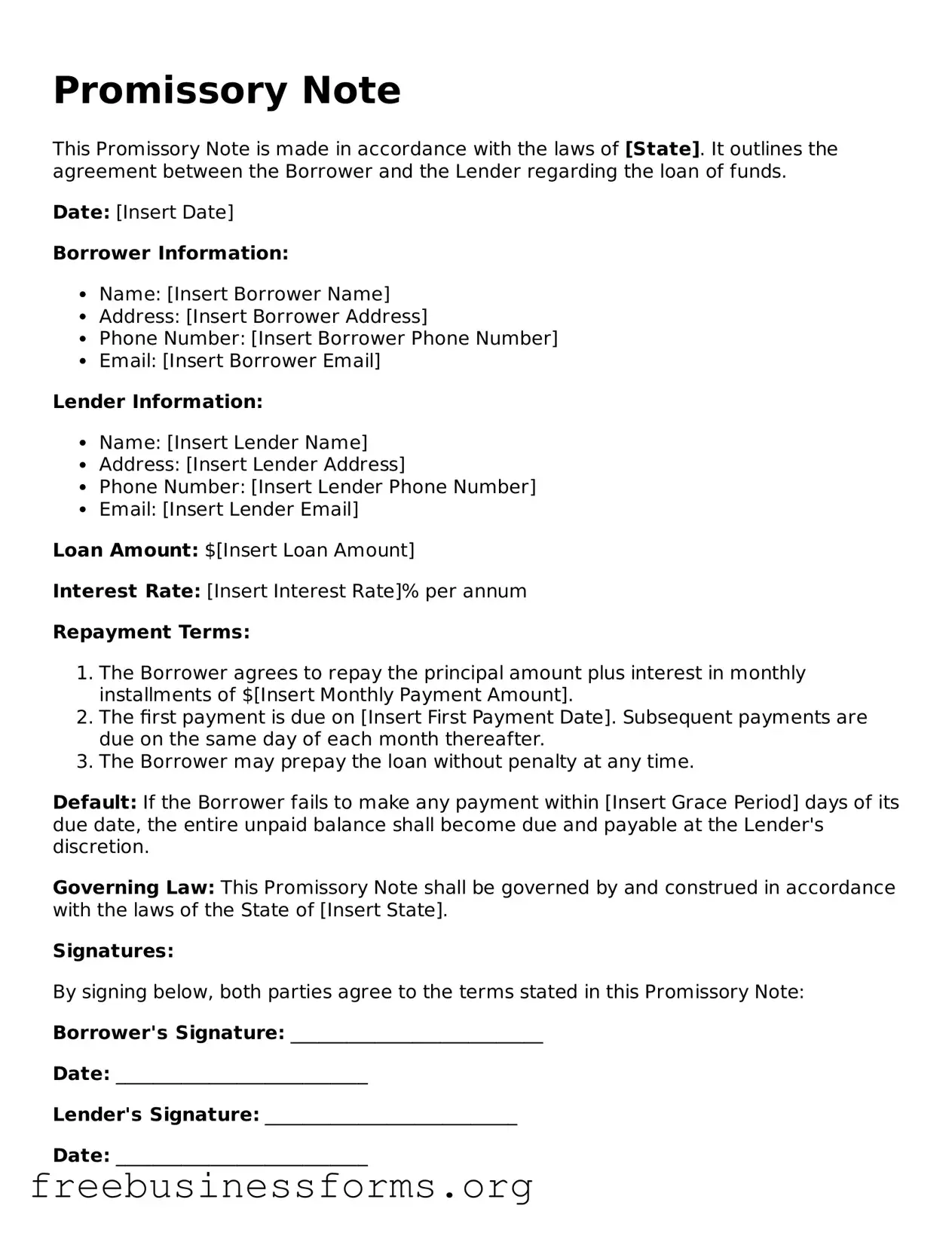

Promissory Note

This Promissory Note is made in accordance with the laws of [State]. It outlines the agreement between the Borrower and the Lender regarding the loan of funds.

Date: [Insert Date]

Borrower Information:

Lender Information:

Loan Amount: $[Insert Loan Amount]

Interest Rate: [Insert Interest Rate]% per annum

Repayment Terms:

Default: If the Borrower fails to make any payment within [Insert Grace Period] days of its due date, the entire unpaid balance shall become due and payable at the Lender's discretion.

Governing Law: This Promissory Note shall be governed by and construed in accordance with the laws of the State of [Insert State].

Signatures:

By signing below, both parties agree to the terms stated in this Promissory Note:

Borrower's Signature: ___________________________

Date: ___________________________

Lender's Signature: ___________________________

Date: ___________________________

| Fact Name | Description |

|---|---|

| Definition | A promissory note is a written promise to pay a specified amount of money to a designated party at a defined time or on demand. |

| Key Components | It typically includes the principal amount, interest rate, maturity date, and the signatures of the borrower and lender. |

| Legal Status | In the U.S., promissory notes are legally enforceable contracts under state law. |

| Governing Law | Each state has its own laws governing promissory notes, often found in the Uniform Commercial Code (UCC). |

| Types | There are two main types: secured notes, which are backed by collateral, and unsecured notes, which are not. |

| Transferability | Promissory notes can be transferred to another party, allowing for flexibility in transactions. |

| Default Consequences | If the borrower fails to repay, the lender may take legal action to recover the owed amount. |

| Interest Rates | Interest rates on promissory notes can vary widely and are often determined by market conditions and negotiations between the parties. |